Exploring Historical Global Temperatures

Tags: Jupyter Notebook Python Time SeriesThe original Jupyter notebook can be viewed here.

This is a time series modeling exercise based on the Kaggle dataset Climate Change: Earth Surface Temperature Data. The raw data comes from the Berkeley Earth data page.

Here I use ‘LandAverageTemperature’ from the dataset Global Land and Ocean-and-Land Temperatures (GlobalTemperatures.csv):

- Date: starts in 1750 for average land temperature and 1850 for max and min land temperatures and global ocean and land temperatures

- LandAverageTemperature: global average land temperature in celsius

- LandAverageTemperatureUncertainty: the 95% confidence interval around the average

- LandMaxTemperature: global average maximum land temperature in celsius

- LandMaxTemperatureUncertainty: the 95% confidence interval around the maximum land temperature

- LandMinTemperature: global average minimum land temperature in celsius

- LandMinTemperatureUncertainty: the 95% confidence interval around the minimum land temperature

- LandAndOceanAverageTemperature: global average land and ocean temperature in celsius

- LandAndOceanAverageTemperatureUncertainty: the 95% confidence interval around the global average land and ocean temperature

In this notebook, I will:

- Import and examine the data from the CSV file

- Model the data using an ARIMA model

- Make predictions with the fitted model

- Compare the performance of this ARIMA model with some baseline models

Importing and Examining the Data

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import statsmodels.api as sm

import scipy.stats as stats

%matplotlib inline

global_temp = pd.read_csv('GlobalTemperatures.csv')

Set the date to be the index, and drop NA values.

Here I only used data starting from 1850, because I am not sure whether the data before 1850 was collected with the same method.

global_temp['dt'] = pd.to_datetime(global_temp['dt'])

global_temp.set_index('dt', inplace = True)

global_temp.dropna(how = 'any', inplace = True)

global_temp.head()

| LandAverageTemperature | LandAverageTemperatureUncertainty | LandMaxTemperature | LandMaxTemperatureUncertainty | LandMinTemperature | LandMinTemperatureUncertainty | LandAndOceanAverageTemperature | LandAndOceanAverageTemperatureUncertainty | |

|---|---|---|---|---|---|---|---|---|

| dt | ||||||||

| 1850-01-01 | 0.749 | 1.105 | 8.242 | 1.738 | -3.206 | 2.822 | 12.833 | 0.367 |

| 1850-02-01 | 3.071 | 1.275 | 9.970 | 3.007 | -2.291 | 1.623 | 13.588 | 0.414 |

| 1850-03-01 | 4.954 | 0.955 | 10.347 | 2.401 | -1.905 | 1.410 | 14.043 | 0.341 |

| 1850-04-01 | 7.217 | 0.665 | 12.934 | 1.004 | 1.018 | 1.329 | 14.667 | 0.267 |

| 1850-05-01 | 10.004 | 0.617 | 15.655 | 2.406 | 3.811 | 1.347 | 15.507 | 0.249 |

global_temp['LandAverageTemperature'].tail()

dt

2015-08-01 14.755

2015-09-01 12.999

2015-10-01 10.801

2015-11-01 7.433

2015-12-01 5.518

Name: LandAverageTemperature, dtype: float64

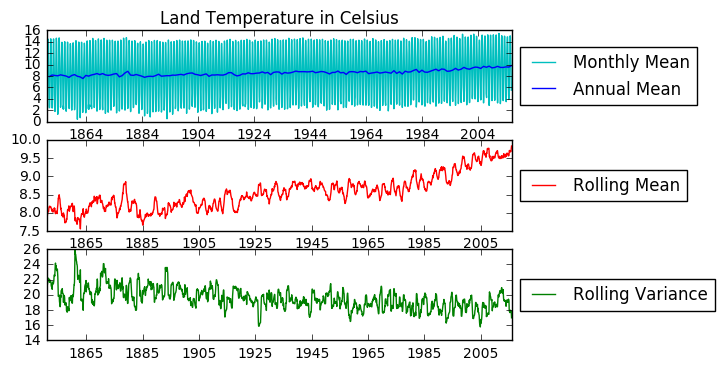

A quick look at the land average temperature data. I am especially interested in seeing whether this time series is stationary.

Augmented Dickey-Fuller unit root test: H0: there is a unit root, ie. non-stationary Ha: there is no unit root (usually equivalent to stationarity or trend stationarity)

fig = plt.figure()

plt.subplot(311)

plt.title('Land Temperature in Celsius')

plt.plot(global_temp['LandAverageTemperature'], color = 'c', label = 'Monthly Mean')

plt.plot(global_temp['LandAverageTemperature'].resample('A').mean(), color = 'b', label = 'Annual Mean')

plt.legend(loc='center left', bbox_to_anchor=(1.0, 0.5))

# Adding rolling mean

rolmean = pd.rolling_mean(global_temp['LandAverageTemperature'], window=12)

rolvar = pd.rolling_var(global_temp['LandAverageTemperature'], window=12)

plt.subplot(312)

plt.plot(rolmean, label = 'Rolling Mean', color = 'r')

plt.legend(loc='center left', bbox_to_anchor=(1.0, 0.5))

plt.subplot(313)

plt.plot(rolvar, label = 'Rolling Variance', color = 'g')

plt.legend(loc='center left', bbox_to_anchor=(1.0, 0.5))

plt.show()

# Augmented Dickey-Fuller Test for stationarity.

def stationarity_test(s, name = None):

if name != None:

print('Results of Dickey-Fuller Test on %s:'%name)

else:

print('Results of Dickey-Fuller Test:')

df_test = sm.tsa.stattools.adfuller(s)

df_result = pd.Series(df_test[0:4], index=['Test Statistic','p-value','#Lags Used','Number of Observations Used'])

for key,value in df_test[4].items():

df_result['Critical Value (%s)'%key] = value

print(df_result)

stationarity_test(global_temp['LandAverageTemperature'], 'Monthly Mean')

Results of Dickey-Fuller Test on Monthly Mean:

Test Statistic -1.455328

p-value 0.555483

#Lags Used 26.000000

Number of Observations Used 1965.000000

Critical Value (5%) -2.863012

Critical Value (1%) -3.433682

Critical Value (10%) -2.567554

dtype: float64

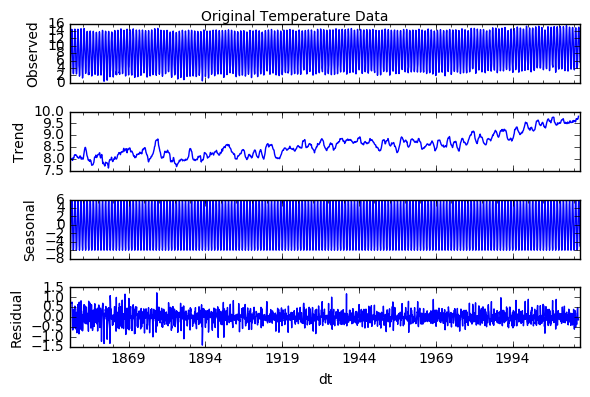

decomposition = sm.tsa.seasonal_decompose(global_temp['LandAverageTemperature'], model='additive')

fig = plt.figure()

fig = decomposition.plot()

plt.suptitle('Original Temperature Data')

<matplotlib.text.Text at 0x7f92afc49b70>

<matplotlib.figure.Figure at 0x7f92afc49080>

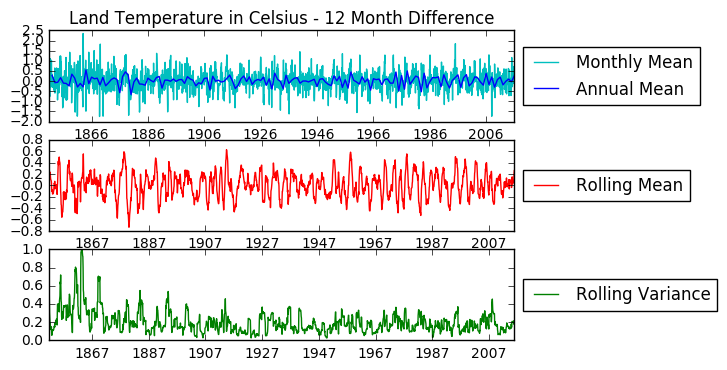

This data is not stationary. It has an upward trend and strong seasonality. Thus I will first attempt to remove seasonality. As seen below, a seasonal (12 months) difference alone makes the stationarity test statistic smaller than the 1% critical values.

temp_diff12 = global_temp['LandAverageTemperature'] - global_temp['LandAverageTemperature'].shift(12)

temp_diff12.dropna(inplace = True)

stationarity_test(temp_diff12, 'Temperature - 12 Month Difference')

Results of Dickey-Fuller Test on Temperature - 12 Month Difference:

Test Statistic -1.278337e+01

p-value 7.334162e-24

#Lags Used 2.400000e+01

Number of Observations Used 1.955000e+03

Critical Value (5%) -2.863020e+00

Critical Value (1%) -3.433699e+00

Critical Value (10%) -2.567558e+00

dtype: float64

fig = plt.figure()

plt.subplot(311)

plt.title('Land Temperature in Celsius - 12 Month Difference')

plt.plot(temp_diff12, color = 'c', label = 'Monthly Mean')

plt.plot(temp_diff12.resample('A').mean(), color = 'b', label = 'Annual Mean')

plt.legend(loc='center left', bbox_to_anchor=(1.0, 0.5))

# Adding rolling mean

rolmean = pd.rolling_mean(temp_diff12, window=12)

rolvar = pd.rolling_var(temp_diff12, window=12)

plt.subplot(312)

plt.plot(rolmean, label = 'Rolling Mean', color = 'r')

plt.legend(loc='center left', bbox_to_anchor=(1.0, 0.5))

plt.subplot(313)

plt.plot(rolvar, label = 'Rolling Variance', color = 'g')

plt.legend(loc='center left', bbox_to_anchor=(1.0, 0.5))

plt.show()

Now the data is stationarized, we can proceed to data modeling.

Modeling the Data (Seasonal ARIMA)

The autoregressive integrated moving average (ARIMA) model is a model often used for analyzing time series data. In this notebook, I will try to use an ARIMA model to model the temperature data above, and use the model to predict the temperatures within and out of the time range of this historical data.

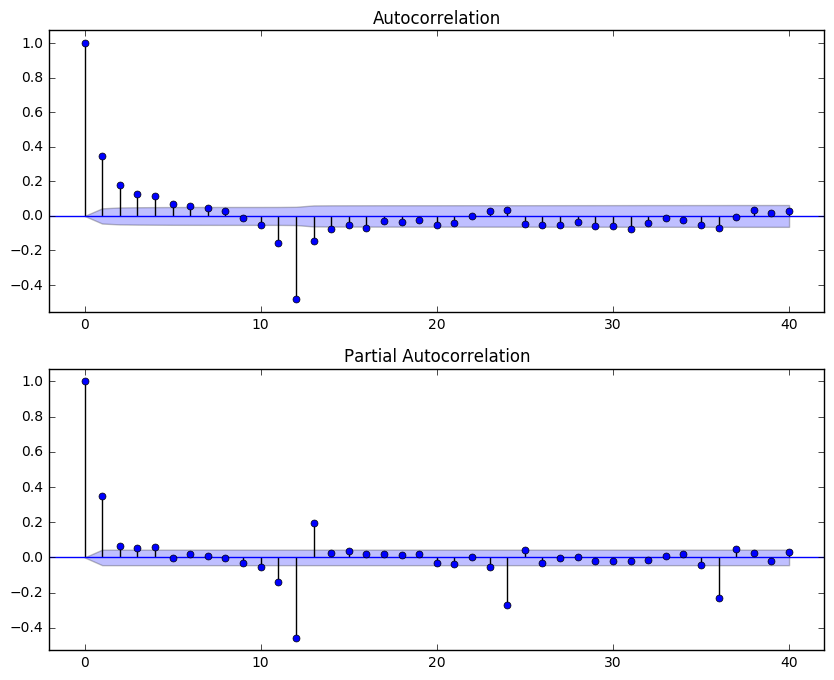

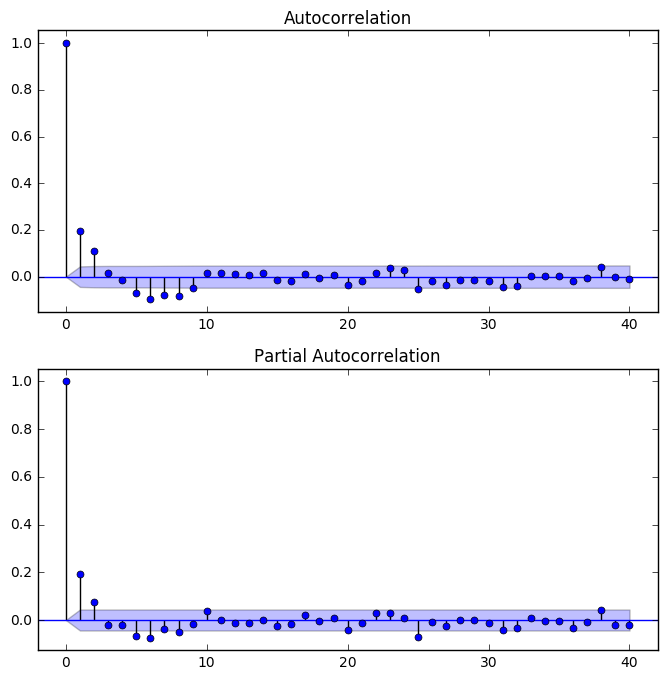

I start by examining the ACF and PACF plots of the seasonal differentiated data:

fig = plt.figure(figsize = (10, 8))

ax1 = fig.add_subplot(211)

fig = sm.graphics.tsa.plot_acf(temp_diff12, lags=40, ax=ax1)

ax2 = fig.add_subplot(212)

fig = sm.graphics.tsa.plot_pacf(temp_diff12, lags=40, ax=ax2)

The seasonal part of the model has a MA(1) term, since there is a spike at lag 12 in the ACF but no other significant spikes, and the PACF shows exponential decay at lag 12x. The non-seasonal part has a AR(2) term, but the MA term is less obvious. After experimenting with the non-seasonal MA term below, I decided the ARIMA(2,0,2)(0,1,1)12 gives the best results. (The experimenting code is commentted out in order to save some run time of this notebook.)

# mod000 = sm.tsa.statespace.SARIMAX(global_temp['LandAverageTemperature'], order=(0,0,0),

# seasonal_order=(0,1,1,12), enforce_stationarity = False,

# enforce_invertibility = False).fit()

# mod201 = sm.tsa.statespace.SARIMAX(global_temp['LandAverageTemperature'], order=(2,0,1),

# seasonal_order=(0,1,1,12), enforce_stationarity = False,

# enforce_invertibility = False).fit()

# mod202 = sm.tsa.statespace.SARIMAX(global_temp['LandAverageTemperature'], order=(2,0,2),

# seasonal_order=(0,1,1,12), enforce_stationarity = False,

# enforce_invertibility = False).fit()

# mod205 = sm.tsa.statespace.SARIMAX(global_temp['LandAverageTemperature'], order=(2,0,5),

# seasonal_order=(0,1,1,12), enforce_stationarity = False,

# enforce_invertibility = False).fit()

# print('Model', 'AIC', 'BIC', 'HQIC')

# for i in range(4):

# mods = [mod000, mod201, mod202, mod205]

# mod_names = ['(0,0,0)', '(2,0,1)', '(2,0,2)', '(2,0,5)']

# print('ARIMA' + mod_names[i] + 'x(0,1,1)_12', mods[i].aic, mods[i].bic, mods[i].hqic)

## Out:

## Model AIC BIC HQIC

## ARIMA(0,0,0)x(0,1,1)_12 1718.88434628 1730.07813515 1722.99530443

## ARIMA(2,0,1)x(0,1,1)_12 1258.33364589 1286.31811808 1268.61104126

## ARIMA(2,0,2)x(0,1,1)_12 1249.70453329 1283.28589992 1262.03740774

## ARIMA(2,0,5)x(0,1,1)_12 1259.46169646 1309.8337464 1277.96100813

mod202 = sm.tsa.statespace.SARIMAX(global_temp['LandAverageTemperature'], order = (2, 0, 2),

seasonal_order=(0,1,1,12), enforce_stationarity = False,

enforce_invertibility = False).fit()

print('Model', 'AIC', 'BIC', 'HQIC')

print('ARIMA(2,0,2)x(0,1,1)_12', mod202.aic, mod202.bic, mod202.hqic)

Model AIC BIC HQIC

ARIMA(2,0,2)x(0,1,1)_12 1249.70453329 1283.28589992 1262.03740774

print(mod202.summary())

Statespace Model Results

==========================================================================================

Dep. Variable: LandAverageTemperature No. Observations: 1992

Model: SARIMAX(2, 0, 2)x(0, 1, 1, 12) Log Likelihood -618.852

Date: Thu, 02 Mar 2017 AIC 1249.705

Time: 13:24:21 BIC 1283.286

Sample: 01-01-1850 HQIC 1262.037

- 12-01-2015

Covariance Type: opg

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

ar.L1 1.5565 1.69e+05 9.22e-06 1.000 -3.31e+05 3.31e+05

ar.L2 -0.5577 2.01e+05 -2.77e-06 1.000 -3.94e+05 3.94e+05

ma.L1 -1.2120 1.11e-08 -1.09e+08 0.000 -1.212 -1.212

ma.L2 0.2372 4.39e-09 5.4e+07 0.000 0.237 0.237

ma.S.L12 -0.9517 5.26e-09 -1.81e+08 0.000 -0.952 -0.952

sigma2 0.1086 2.58e-08 4.21e+06 0.000 0.109 0.109

===================================================================================

Ljung-Box (Q): 58.65 Jarque-Bera (JB): 285.74

Prob(Q): 0.03 Prob(JB): 0.00

Heteroskedasticity (H): 0.55 Skew: 0.13

Prob(H) (two-sided): 0.00 Kurtosis: 4.85

===================================================================================

Warnings:

[1] Covariance matrix calculated using the outer product of gradients.

[2] Covariance matrix is singular or near-singular, with condition number 2.56e+43. Standard errors may be unstable.

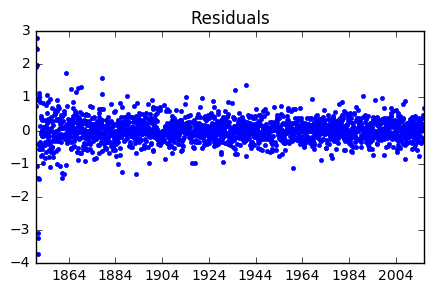

Now I analyze the residuals of the ARIMA(2,0,2)x(0,1,1)_12 model.

fig = plt.figure(figsize = (5, 3))

resid202 = mod202.resid

plt.plot(resid202, 'b.')

plt.title('Residuals')

plt.show()

fig = plt.figure(figsize = (8, 8))

ax1 = fig.add_subplot(211)

fig = sm.graphics.tsa.plot_acf(resid202, lags=40, ax=ax1)

ax2 = fig.add_subplot(212)

fig = sm.graphics.tsa.plot_pacf(resid202, lags=40, ax=ax2)

Neither the ACF or PACF plots of the residuals showed any spikes beside lag 0, indicating the residuals are not autocorrelated.

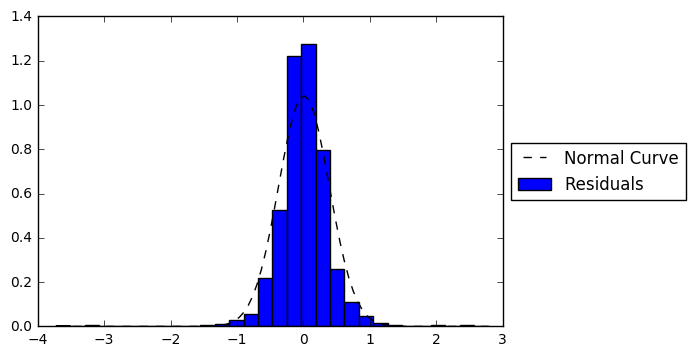

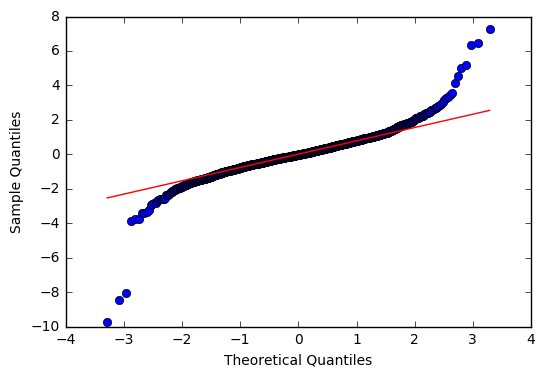

For the normal test below, the H0 is that a sample comes from a normal distribution.

def fit_norm(data):

'''Fits a Normal distribution to 1D data.'''

mu, std = stats.norm.fit(data)

x = np.linspace(np.min(data),np.max(data),100)

y = stats.norm.pdf(x, mu, std)

return (x, y)

plt.figure()

plt.hist(resid202, bins = 30, normed = True, label = 'Residuals')

x, y = fit_norm(resid202)

plt.plot(x, y,'k--', label = 'Normal Curve')

plt.legend(loc='center left', bbox_to_anchor=(1.0, 0.5))

plt.show()

print(stats.normaltest(resid202))

NormaltestResult(statistic=463.76425536589068, pvalue=1.9718391964105937e-101)

fig = plt.figure()

ax = sm.graphics.qqplot(resid202, line='q', fit=True)

<matplotlib.figure.Figure at 0x7f92addf8278>

From the normal test and the Q-Q plot, we can see the residuals are heavy tailed.

Making Predictions

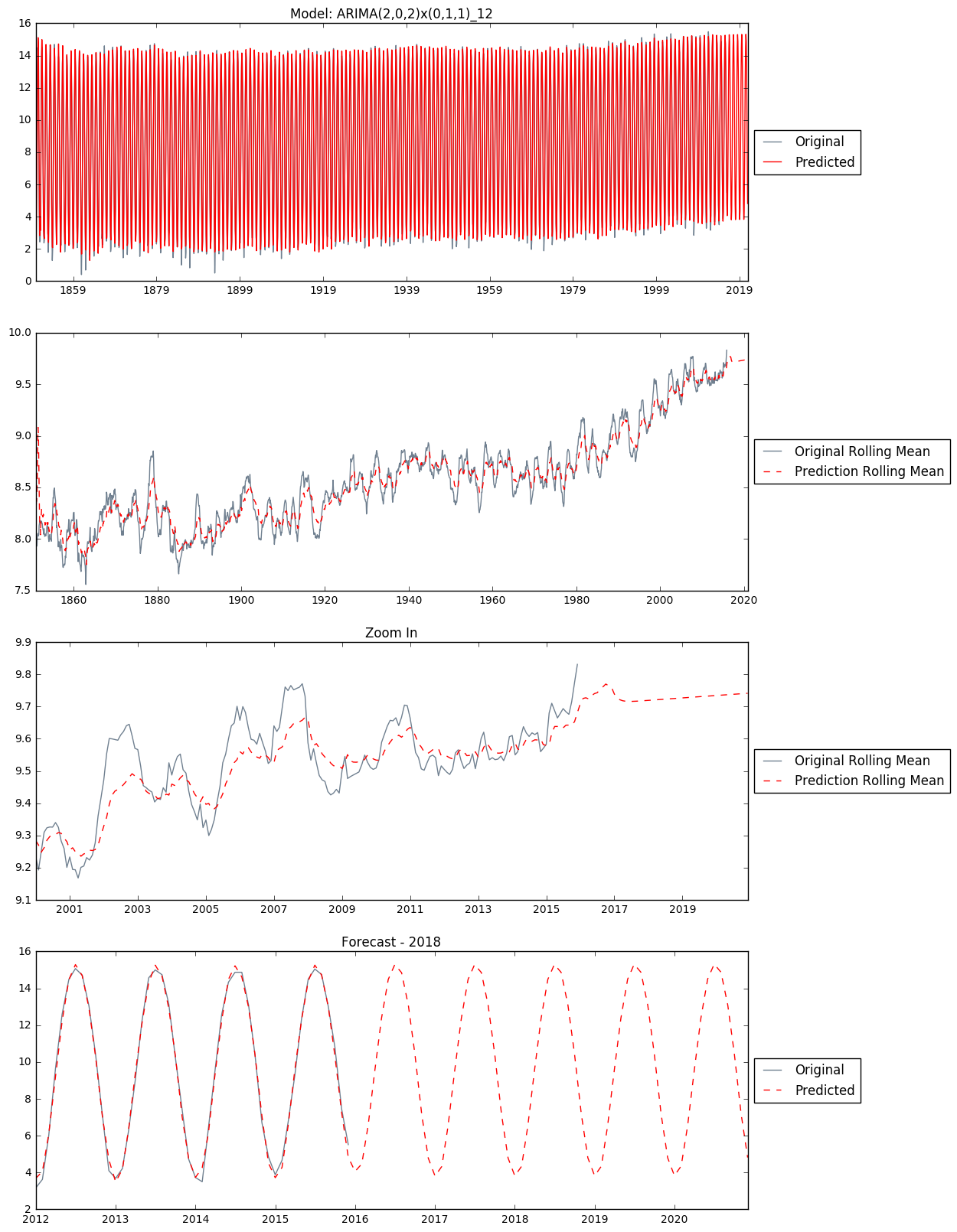

I use this ARIMA(2,0,2)x(0,1,1)_12 model from above to make in-sample and out-of-sample predictions. The date of last entry in the historical data is 2015-12-01. We will make a five year prediction afterwards only for the sake of learning. Of courese in reality, five-year-ahead weather prediction is almost guaranteed unrealiable.

predict_mod202 = mod202.predict('1850-01-01', '2020-12-01')

fig, axs = plt.subplots(4, figsize = (12, 20))

axs[0].set_title('Model: ARIMA(2,0,2)x(0,1,1)_12')

axs[0].plot(global_temp['LandAverageTemperature'], color = 'slategray', label = 'Original')

axs[0].plot(predict_mod202, color = 'red', label = 'Predicted')

axs[0].legend(loc='center left', bbox_to_anchor=(1.0, 0.5))

predict_rolmean = pd.rolling_mean(predict_mod202, window=12)

original_rolmean = pd.rolling_mean(global_temp['LandAverageTemperature'], window=12)

axs[1].plot(original_rolmean, color = 'slategray', label = 'Original Rolling Mean')

axs[1].plot(predict_rolmean, color = 'red', linestyle = '--', label='Prediction Rolling Mean')

axs[1].legend(loc='center left', bbox_to_anchor=(1.0, 0.5))

axs[2].set_title('Zoom In')

axs[2].plot(original_rolmean['2000':], color = 'slategray', label = 'Original Rolling Mean')

axs[2].plot(predict_rolmean['2000':], color = 'red', linestyle = '--', label='Prediction Rolling Mean')

axs[2].legend(loc='center left', bbox_to_anchor=(1.0, 0.5))

axs[3].set_title('Forecast - 2018')

axs[3].plot(global_temp['LandAverageTemperature']['2012':'2020'], color = 'slategray', label = 'Original')

axs[3].plot(predict_mod202['2012':'2020'], color='red', linestyle = '--', label = 'Predicted')

axs[3].legend(loc='center left', bbox_to_anchor=(1.0, 0.5))

x, y = fit_norm(resids[i])

Baseline Comparison

Now I have a working model, I would like to see how it compares against some baseline models. Nate Silver mentions in his book “The Signal and the Noise” with respect to weather forecasting:

“There are two basic tests that any weather forecast must pass to demonstrate its merit:

- It must do better than what meteorologists call persistence: the assumption that the weather will be the same tomorrow (and the next day) as it was today.

- It must also beat climatology, the long-term historical average of conditions on a particular date in a particular area.”

Thus I will build these two baseline models accordingly for comparison.

Alt Model 1: Persistence

In this model, each month’s temperature is predicted to be the same as that of the previous month.

predict_dates = pd.date_range(start = '1850-01-01', end ='2020-12-01', freq='MS')

predict_altmod1 = pd.DataFrame(index = predict_dates, columns = ['forecast', 'observed', 'resid'])

predict_altmod1['observed'] = global_temp['LandAverageTemperature']

predict_altmod1['forecast'] = global_temp['LandAverageTemperature'].shift(1)

predict_altmod1.loc['1850-01-01', 'forecast'] = global_temp.loc['1850-01-01', 'LandAverageTemperature']

last_observed = global_temp['LandAverageTemperature'].iloc[-1]

# all out-of-sample predictions are the same as the last temperature entry in the original data set (observed)

predict_altmod1['forecast'].fillna(last_observed, inplace = True)

predict_altmod1['resid'] = predict_altmod1['observed'] - predict_altmod1['forecast']

print(predict_altmod1.head(20))

print(predict_altmod1.tail(20))

forecast observed resid

1850-01-01 0.749 0.749 0.000

1850-02-01 0.749 3.071 2.322

1850-03-01 3.071 4.954 1.883

1850-04-01 4.954 7.217 2.263

1850-05-01 7.217 10.004 2.787

1850-06-01 10.004 13.150 3.146

1850-07-01 13.150 14.492 1.342

1850-08-01 14.492 14.039 -0.453

1850-09-01 14.039 11.505 -2.534

1850-10-01 11.505 8.091 -3.414

1850-11-01 8.091 4.733 -3.358

1850-12-01 4.733 2.803 -1.930

1851-01-01 2.803 2.431 -0.372

1851-02-01 2.431 2.508 0.077

1851-03-01 2.508 4.192 1.684

1851-04-01 4.192 7.287 3.095

1851-05-01 7.287 11.113 3.826

1851-06-01 11.113 13.418 2.305

1851-07-01 13.418 14.531 1.113

1851-08-01 14.531 13.751 -0.780

forecast observed resid

2019-05-01 5.518 NaN NaN

2019-06-01 5.518 NaN NaN

2019-07-01 5.518 NaN NaN

2019-08-01 5.518 NaN NaN

2019-09-01 5.518 NaN NaN

2019-10-01 5.518 NaN NaN

2019-11-01 5.518 NaN NaN

2019-12-01 5.518 NaN NaN

2020-01-01 5.518 NaN NaN

2020-02-01 5.518 NaN NaN

2020-03-01 5.518 NaN NaN

2020-04-01 5.518 NaN NaN

2020-05-01 5.518 NaN NaN

2020-06-01 5.518 NaN NaN

2020-07-01 5.518 NaN NaN

2020-08-01 5.518 NaN NaN

2020-09-01 5.518 NaN NaN

2020-10-01 5.518 NaN NaN

2020-11-01 5.518 NaN NaN

2020-12-01 5.518 NaN NaN

Alt Model 2: Overly Simplified Seasonal

In this model, each month’s temperature is predicted to be the mean of all historical temperatures of the same month of the year. Eg. the predicted temperature of January 2016 would be the mean of all January temperatures from 1851 to 2015; the predicted temperature of February 2017 would be the mean of all February temperatures from 1851 to 2016, and so on.

predict_dates = pd.date_range(start = '1850-01-01', end ='2020-12-01', freq='MS')

df = pd.DataFrame(index = predict_dates, columns = ['forecast', 'observed'])

df['observed'] = global_temp['LandAverageTemperature']

df_list = []

for m in range(1, 13):

newdf = df[df.index.month == m].copy()

newdf['forecast'] = pd.Series.expanding(newdf['observed']).mean()

df_list.append(newdf)

predict_altmod2 = pd.concat(df_list)

predict_altmod2.sort_index(inplace = True)

predict_altmod2['resid'] = predict_altmod2['observed'] - predict_altmod2['forecast']

print(predict_altmod2.head(20))

print(predict_altmod2.tail(20))

forecast observed resid

1850-01-01 0.7490 0.749 0.0000

1850-02-01 3.0710 3.071 0.0000

1850-03-01 4.9540 4.954 0.0000

1850-04-01 7.2170 7.217 0.0000

1850-05-01 10.0040 10.004 0.0000

1850-06-01 13.1500 13.150 0.0000

1850-07-01 14.4920 14.492 0.0000

1850-08-01 14.0390 14.039 0.0000

1850-09-01 11.5050 11.505 0.0000

1850-10-01 8.0910 8.091 0.0000

1850-11-01 4.7330 4.733 0.0000

1850-12-01 2.8030 2.803 0.0000

1851-01-01 1.5900 2.431 0.8410

1851-02-01 2.7895 2.508 -0.2815

1851-03-01 4.5730 4.192 -0.3810

1851-04-01 7.2520 7.287 0.0350

1851-05-01 10.5585 11.113 0.5545

1851-06-01 13.2840 13.418 0.1340

1851-07-01 14.5115 14.531 0.0195

1851-08-01 13.8950 13.751 -0.1440

forecast observed resid

2019-05-01 11.241373 NaN NaN

2019-06-01 13.412976 NaN NaN

2019-07-01 14.370072 NaN NaN

2019-08-01 13.837139 NaN NaN

2019-09-01 11.997157 NaN NaN

2019-10-01 9.334217 NaN NaN

2019-11-01 5.991873 NaN NaN

2019-12-01 3.574060 NaN NaN

2020-01-01 2.547952 NaN NaN

2020-02-01 3.076500 NaN NaN

2020-03-01 5.151518 NaN NaN

2020-04-01 8.324157 NaN NaN

2020-05-01 11.241373 NaN NaN

2020-06-01 13.412976 NaN NaN

2020-07-01 14.370072 NaN NaN

2020-08-01 13.837139 NaN NaN

2020-09-01 11.997157 NaN NaN

2020-10-01 9.334217 NaN NaN

2020-11-01 5.991873 NaN NaN

2020-12-01 3.574060 NaN NaN

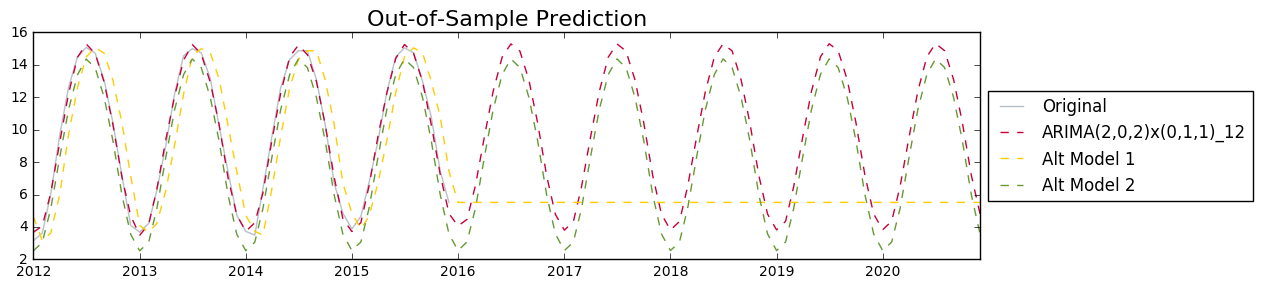

fig = plt.figure(figsize = (10, 3))

mod_names = ['ARIMA(2,0,2)x(0,1,1)_12', 'Alt Model 1', 'Alt Model 2']

predicts = [predict_mod202, predict_altmod1['forecast'], predict_altmod2['forecast']]

colors = ['#c70039', '#FFCC00', '#669933']

plt.plot(global_temp['LandAverageTemperature']['2012':'2020'], color = 'slategray', label = 'Original', alpha = 0.5)

for i in range(3):

plt.plot(predicts[i]['2012':'2020'], color = colors[i], linestyle = '--', label = mod_names[i])

plt.title('Out-of-Sample Prediction', size = 16)

plt.legend(loc='center left', bbox_to_anchor=(1, 0.5))

fig.tight_layout()

plt.show()

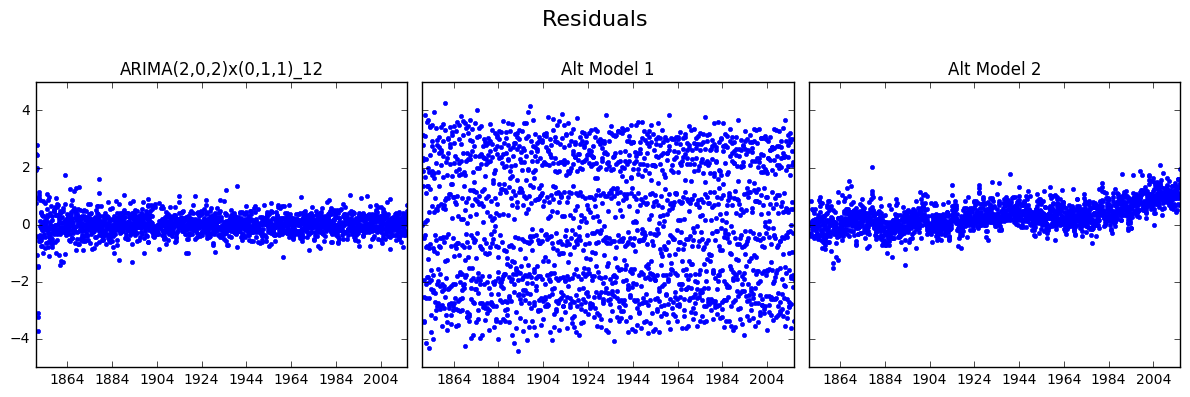

Residual Analysis

fig, axs = plt.subplots(1, 3, sharey = True, figsize = (12, 4))

resids = [resid202, predict_altmod1['resid'].dropna(), predict_altmod2['resid'].dropna()]

for i in range(3):

axs[i].set_title(mod_names[i])

axs[i].plot(resids[i], 'b.')

fig.suptitle('Residuals', size = 16)

fig.tight_layout()

fig.subplots_adjust(top = 0.8)

plt.show()

We can see from the figures above that the Alt Model 1 (Persistence) has very scattered residuals (aka the errors are large). The residuals of Alt Model 2 (Overly Simplified Seasonal) seems to have a upward trend, which is undesirable.

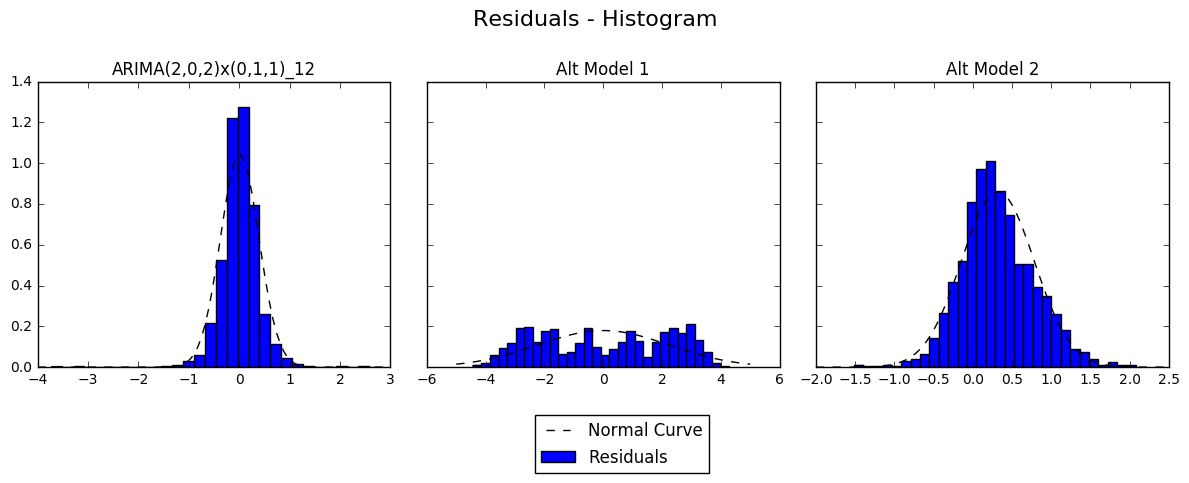

fig, axs = plt.subplots(1, 3, sharey = True, figsize = (12, 4))

for i in range(3):

plt.sca(axs[i])

axs[i].set_title(mod_names[i])

plt.hist(resids[i], bins = 30, normed = True, label = 'Residuals')

x, y = fit_norm(resids[i])

plt.plot(x, y,'k--', label = 'Normal Curve')

print(mod_names[i], stats.normaltest(resids[i]))

fig.suptitle('Residuals - Histogram', size = 16)

plt.legend(loc='lower center', bbox_to_anchor=(-0.55, -0.4))

fig.tight_layout()

fig.subplots_adjust(top = 0.8)

plt.show()

ARIMA(2,0,2)x(0,1,1)_12 NormaltestResult(statistic=463.76425536589068, pvalue=1.9718391964105937e-101)

Alt Model 1 NormaltestResult(statistic=39154.279102240027, pvalue=0.0)

Alt Model 2 NormaltestResult(statistic=43.638821605600526, pvalue=3.3415678972003915e-10)

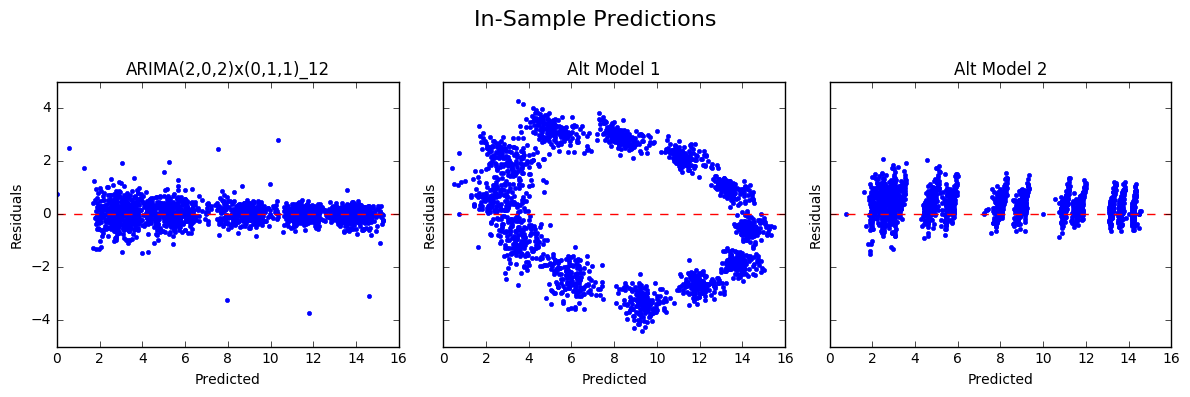

fig, axs = plt.subplots(1, 3, sharey = True, figsize = (12, 4))

for i in range(3):

plt.sca(axs[i])

axs[i].set_title(mod_names[i])

axs[i].set_xlabel('Predicted')

axs[i].set_ylabel('Residuals')

axs[i].plot(predicts[i][:'2015-12-01'], resids[i], 'b.')

plt.axhline(y = 0, color='red', linestyle = '--')

fig.suptitle('In-Sample Predictions', size = 16)

fig.tight_layout()

fig.subplots_adjust(top = 0.8)

plt.show()

In the plots of the residuals against the fitted values above, we can see both of the alternative models showed patterns (again, undesirable), whereas the seasonal ARIMA model produced residuals scattered randomly around the line y = 0 (expected).

Forecast Performance:

I will evaluate the forecast performance of these three model using two of the most commonly used measures, RMSE (root mean squared error) and MAE (mean absolute error).

print('{:<30s}{:<10s}{:<10s}'.format('Model', 'RMSE', 'MAE'))

print('-' * 50)

for i in range(3):

print('{:<30s}{:<10.4f}{:<10.4f}'.format(mod_names[i],

sm.tools.eval_measures.rmse(global_temp['LandAverageTemperature'],

predicts[i][:'2015-12-01']),

sm.tools.eval_measures.meanabs(global_temp['LandAverageTemperature'],

predicts[i][:'2015-12-01'])))

Model RMSE MAE

--------------------------------------------------

ARIMA(2,0,2)x(0,1,1)_12 0.3831 0.2626

Alt Model 1 2.2259 1.9782

Alt Model 2 0.5635 0.4339

Now we are confident that the seasonal ARIMA model out performs both of the baseline models.